The Four Pillars of Venture Investing

Trade-Offs In Everything You Do

This is a weekly newsletter about the art and science of building and investing in tech companies. To receive Investing 101 in your inbox each week, subscribe here:

Life is filled with trade-offs. I've written before about how everyone is an allocator of something "because they’re allocating finite things in their lives: money, attention, time, effort, love."

Supposedly Mark Zuckerberg's sister, Randi Zuckerberg, says the "entrepreneur's dilemma" is that across work, sleep, family, fitness, and friend, you can have three of those five. Trade-offs. If you want to work hard and prioritize sleep, then your family and friends will get deprioritized in favor of fitness If you want to prioritize family and fitness, then your friends and sleep will get sacrificed in favor of work.

As any kid who grew up in the 90's, I immediately started thinking about Aladdin (the cartoon, not the Will Smith embarrassment). Spoiler alert. At the end of the movie, the villain Jafar has been making wishes to make himself more and more powerful. Finally, Aladdin tricks him into wishing to be a genie. And while he does get "unlimited cosmic power," Aladdin reminds him of the consequences of what he wants. "Itty bitty living space."

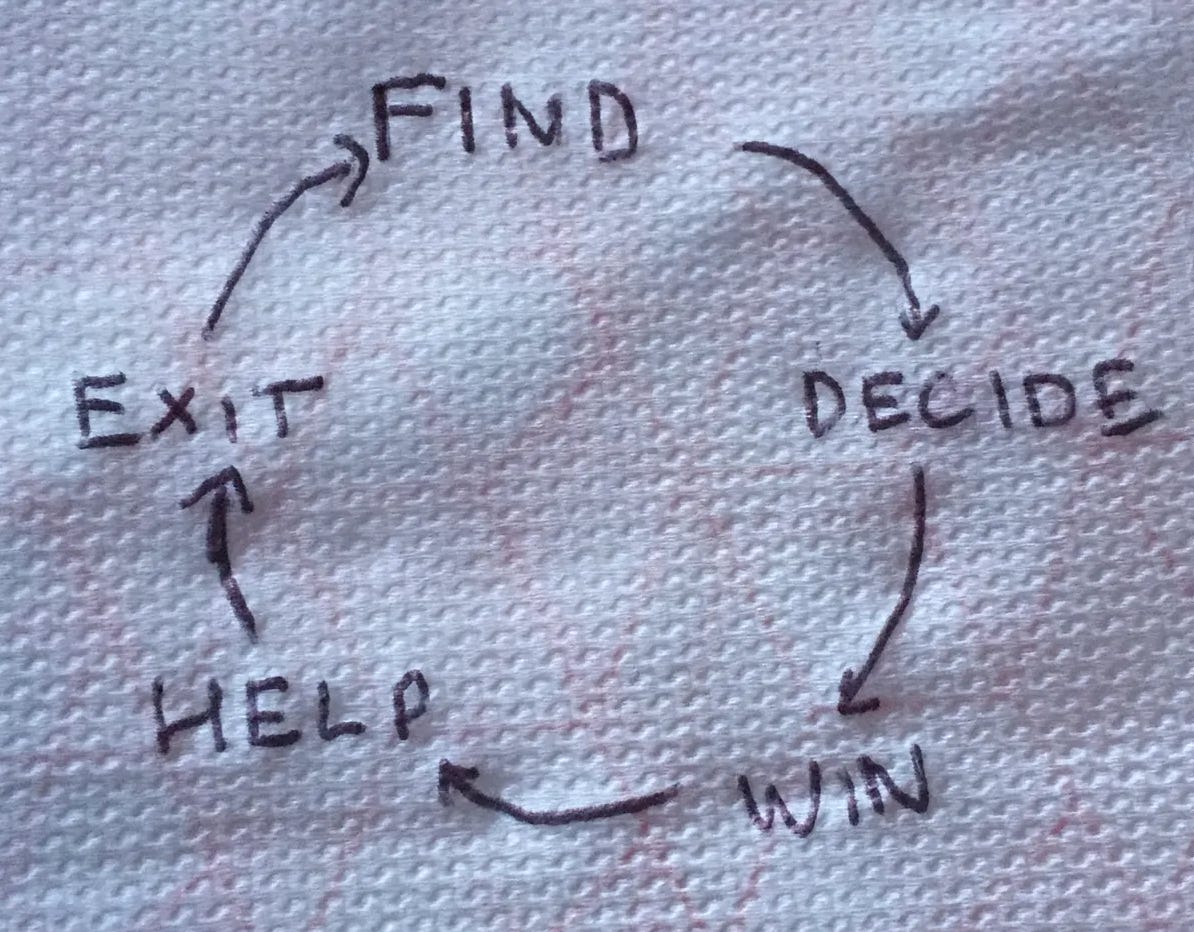

In venture, there are often four key "jobs" of any venture investor. Recently, I was talking with a friend and I started to appreciate just how much trade-offs there are across each of those four jobs that, in some ways, make them nearly mutually exclusive.

In July 2020, my friend Nikhil Trivedi described those jobs as "The Venture Capital Flowchart."

He included a fifth one that I didn't, which is exiting. I have a slightly different perspective that what Nikhil articulates in his excellent piece, which I'll revisit at the end.

The four core jobs of a venture investor, in my mind, are (1) finding, (2) picking, (3) winning, and (4) supporting. I wanted to unpack the four jobs and how they are sometimes at odds with each other.

Finding

Inbound & Outbound

The beginning of any venture investor's usefulness begins with Finding. This is a part of the puzzle that is close to my heart because, like a lot of people, I grew up at a firm where finding, or "sourcing" was an intensely prioritized part of the culture. Firms like TCV, Insight, Bessemer, Summit — even more than other firms they prioritize the importance of sourcing as part of the job.

But it's also a very unique type of sourcing. Building pipeline, chasing leads, following up. It's just like an outbound sales motion. We tracked "touches" with a company, assigned names in a pipeline, and had a pipeline review meeting every Monday. At TCV I was younger in my career, so I was covering ~8K companies that I was trying to prioritize, having 100+ calls with companies per month.

Side note, but I also think people who have served Mormon missions are uniquely comfortable with this part of the job. When I served for two years trying to find people to teach about Jesus, I did something similar. I planned specific time for "finding" where I was knocking on doors. I tracked which neighborhoods I had covered before, I recorded names of "Potentials" in my daily planner. Also why Mormons are good at sales generally. 😉

But pipeline building isn't the only kind of sourcing investors do.

Some focus heavily on plugging into specific ecosystems and investing in those people, whether its shared alumni networks, or people coming out of the same companies ala Paypal Mafia. Others focus on things like academic track records, which has become even more prevalent as AI has come to dominate the startup stage.

Then there is inbound Finding. Rather than who are you going after, it's about who is coming looking for you. This comes from a lot of brand building and reputation management. Some exceptional investors have built their entire track record off inbound investing. Whether its a reputation as an operator or influencer more broadly.

Heat Seeking

One of the obstacles in Finding in modern venture is that it's SO noisy. No longer is it likely that you would be a founder, just minding your own business, and some scrappy investor tracked you down to your Mom's garage. If you start something, EVERYONE knows about it. It's louder than ever.

As a result, heat seeking has become dramatically more prevalent. I've met some pretty exceptional heat seekers in my career. These are folks who seem to just have a nose for what everyone is talking about. When companies have hit some impressive milestone, or a highly sought after co-founder has joined a particular startup. And then they chase that.

One negative aspect of this style of sourcing is that often, though not always, it can be the most shallow part of the job.

"What does the company do?"

Heat Seeker: "It's a hot company."

"What's their business model?"

Heat Seeker: "To be hot."

"How do they differentiate from Competitor XYZ?"

Heat Seeker: "By being hotter."

You don't ask a heat seeking missile about the characteristics of its target; it has one focus: heat.

Awareness

A lot of firms have circled around this idea of wanting to see everything. That idea is built around the idea that venture is focused more on sins of omission than commission. Every investor knows they're going to make mistakes. They are absolutely going to pass on some things that go on to crush, and they are most definitely going to invest in things that totally fizzle.

But what the model cannot abide is not having the opportunity to make a decision. Not seeing something is the cardinal sin. As a result, venture investors have become borderline rabid in their pursuit of "seeing it all." Awareness is a currency in venture investing.

That hunger for awareness has given rise to what I often call the "whisper economy of venture capital," where every junior person is trafficking in gossip about specific deals / companies from other junior people, and senior people are doing the same thing with their senior colleagues. The whisper economy is often framed as "giving your fellow investors a look."

Whether its programmatic inbound and outbound efforts, more haphazard heat seeking, or weaponizing the whisper economy, Finding is the starting gun for any venture investor.

Picking

Early Qualification

Once you find a company worth paying attention to, the work has only just begun. The question is whether this is a company worth investing in.

One of the weaknesses of heavy sourcing cultures in a firm is that success is so heavily tied to Finding that it clouds people's judgement. If an investor is heavily incentivized on finding something, then they translate that into success. And once they find something, they think the job is done.

Particularly among junior people, and Heat Seekers, they take great pride in the companies they find. So they just want to jump straight from Finding to Winning. But this is an automatic recipe for a bad portfolio. Not every company worth Finding is worth investing in.

More often, experienced investors are more likely to fall victim to what I've written about before, called The Groucho Marx Mandate. Tenured investors are skeptical of founders who want to work with them. If a founder is too eager, a VC's mental radar might go off, "what's wrong with this company? Why did other people pass?"

Early qualification takes into account how we found the company, what the details are, and how it fits into our mental model of what we've seen before. A combination of team quality, early traction, design partners, or idea quality will determine how seriously an investor takes an idea.

I've written A LOT about hype cycles and FOMO, and this is often where that muscle kicks in for most VC monkey brains. Yes, they'll look at the details of the company, but The Bubble Brains of Silicon Valley are often just as interested, if not more interested, in what other people think.

Group-Think

When I wrote my Bubble Brains piece a little over a year ago, it was spurred by a conversation I had with a friend who expressed this sentiment:

"It's gloomy out there, man. There is no original thinking among the funds in San Francisco. I don’t know what constitutes a “hot deal.” Because they got a term sheet from Sequoia?"

The group-think in venture investing is a phenomenon so multi-faceted and complex, it deserves to be studied by sociologists.

Granted, many firms will say they are independent thinkers and make decisions before other firms do. But, come "Valentine's Day" for a specific deal, a lot of investors feel this way:

Every firm, every investor, every deal exists on a spectrum. From how much an investor is weighing the merits of the opportunity vs. how much an investor is weighing the interest of other investors.

It reminds me an idea about efficient market theory. Increasingly, the public market is becoming more irrational (see: Meme Stocks). Some people think you're trying to determine what a particular stock price will do. But that's not quite right. You're actually trying to determine what you think other people think a stock price will do. The impact of human psychology on the particular investment is a quantifiable delta that can't be ignored. The same is the most true it could be in venture capital.

Winning

Whether you found an opportunity through thoughtful thesis-driven specialization or good ol' fashioned heat seeking. Whether you decided you wanted to invest through measured, unemotional diligence or rabid FOMO at the mouth. You've decided. Now? You have to get the opportunity to reciprocate.

Granted, maybe some companies only have one choice. Once you decide you want to invest, they say yes. But that happens rarely, and increasingly its more and more rare. FOMO and group-think have made it much more likely that you'll either have no choices or several choices.

As a result, when a company has been weighed and measured by the investor apparatus, and determined to be "hot" or at the very least, "investable," then the question is whether the founder will pick you. Why are they going to pick your money that is just as green as everyone else's?

In my experience, winning deals often comes down to how an investor measures up on a particular scorecard that a founder is filling out in their heads: (1) making the pie bigger, (2) the airport test, and (3) staying out of my way.

Making The Pie Bigger

Chris Sacca has a great line about taking money. The only reason you should raise capital is if you think the addition of the person's money will ultimately make the pie bigger. If you can build a $1B pie and own 100% or 80% either way, you would rather have 100% right? But if you could own 100% of a $200M pie or 80% of a $1B pie, then you want the latter, so you take the money.

Every founder is weighing an investor for how much they'll help them make the overall pie bigger. And that encapsulates a lot of "value add."

Help with hiring, help with customers, help with downstream capital, help with regulatory issues. All of it is woven into a question of how much a particular firm is going to help the founder make their pie bigger.

The Airport Test

The reality in our world of industrialized capital is that there are quite a firms who probably offer equivalent ability to "make the pie bigger." So once you've solved for whether that particular firm will help with the pie growing that you think is most important in the near term, then it gets more personal.

Founders apply the airport test. "Would I want to be stuck in the airport with this person for hours?" For some people, they have long established relationships with the investors they end up raising from. Other times, they met them at the beginning of a fundraising process, and two weeks later have to decide whether they want to go on a decade-long journey together.

Who you are, as a person, can often be the difference between winning or losing a deal.

Side note: I'd like to say that means that assholes don't win but... they do. That's worth some reflection as an industry, both from founders and investors.

Staying Out Of The Way

Over the last few years, founders have started to prioritize another aspect of qualifying an investor. “I want help and support, but I don't want them meddling.” Look at Bench Accounting for a recent example of what happens when founders and investors butt heads. Or Travis Kalanick and Uber as a much more dramatic example.

An investor might pass the airport test, but there is a big difference in someone when they're out for drinks with you vs. if they're negotiating a ratchet clause in a future funding round forcing you to anchor yourself to specific milestones.

Building a reputation as an investor that isn't trying to run a company over top of a founder is important. I wrote about one possible example back in August 2022 where, maybe, a16z writing a $300M check for Adam Neumann's company was almost like a $300M marketing expense. a16z had historically gotten a black eye when they fired Parker Conrad from Zenefits; that came back to bite them when he rose again and built Rippling. Maybe backing Adam Neumann is a16z's way of saying, "but no, really, we support founders even after they've been disgraced and destroyed billions in value." Who knows.

Supporting

Finally, you get to the end of the "transactional" part of the journey and progress into the stuff that actually takes up the bulk of the relationship, ironically. It's funny that every venture deal is typically the beginning of a decades-long journey but the decision to get into that relationship might take a few weeks, tops.

Supporting a company is where the rubber meets the road and a VC actually puts up or shuts up. Though, unfortunately, a lot of VCs find themselves neither putting up nor shutting up. As Vinod Khosla says:

"90% of investors add no value, in my assessment, and 70% of investors add negative value to a company."

The "stay out of my way" heuristic founders are looking for is, in large part, driven by the fear of finding themselves having taken money from someone in the 70% of investors who are going to destroy value in the company. Whether its bad advice, or willful ignorance of what is most important for the company.

Even among investors who have proven to be good supporters, typically as board members, there is a limit to that capacity.

One good metric to use for a founder in measuring whether you should pick a particular investor is how many board seats they have. Because the more board seats they have, the less time they're going to have for you. That, on top of the fact that they still want to keep the rest of the cycle alive; finding, picking, and winning more.

Becoming good at supporting a company is also the part of the job that typically takes the longest to get good at, if you even ever do. Even former operators, including former CEOs and founders, can struggle with this part of the job. I've known former founders who became VCs and were self-aware enough to acknowledge that they have to actively prevent their instincts from taking over.

What I mean by that is if you've been a founder then you know how YOU would run a company. But as an investor, being Supportive doesn't mean taking over and doing it your way. It means supporting a founder in doing it their way. And for someone who has had their hands on the reins for a decade plus, that can be hard to do.

The Consequences of What You Want

Those are the big jobs of a venture investor. Finding, picking, winning, and supporting. Easy enough, right?

Here's why I started this piece talking about trade-offs. I've always loved a talk by Neal Maxwell where he gave me one of the great lines I use a lot (especially as a parent):

"You had better want the consequences of what you want."

You can WANT to be a good "Finder." But if you're a heat seeker who is focused on what is hot, what everyone is thinking about, then you're likely not a very good "Picker."

You can WANT to be a good "Picker." But that can include a lot of really thoughtful diligence where you want to turn over every stone and ask every question. But in a competitive market, founders may be optimizing for whose diligence process is going to be the least onerous, so you might struggle to be a good "Winner."

You can WANT to be a good "Winner." But winning requires being driven by the thrill of the hunt. You hunger for the competitive sparring in getting to the deal, and pulling out all the stops to win. I've heard VCs describe themselves as "addicted to winning" with Michael Jordan as their kindred spirit. But the more you're chasing the next win, the less you're focused on your last win, which makes you not a very good "Supporter."

You can WANT to be a good "Supporter." But supporting startups takes time. It's emotionally draining, and often your worst investments take up the most of your time. And you can roll up your sleeves, and want to spend a ton of time with your companies. People say VCs build their reputations in those instances where support is hugely needed. But all the time you're spending supporting your existing companies, means you're not finding new companies. So it makes it harder for you to be a good "Finder."

Just like any act of allocation; you're allocating a finite resource. And your time is a finite resource. So, as a venture investor, you have a finite amount of time and attention that you have to allocate to finding, picking, winning, or supporting. And you can say "I'm just going to be a good Finder," but if that's your approach you better (1) be at a firm with good pickers, winners, and supporters, and (2) be at a firm that is willing to let you just be a good Finder.

You likely can't be the best in the world at Finding, Picking, Winning, AND Supporting. But you won't survive if you're not at least passable at some of them, and you won't succeed in the long-run if you're not exceptional in at least 2-3 of them. That's the Funder's Dilemma.

Raising & Riding

Final note. I mentioned that Nikhil includes exiting in his flywheel. But I would segment this as a critical, but separate, part of the venture capital process. I think of it that way for the same reason that fundraising isn't one of the key jobs, even though it is just as critical.

I've written a LOT about the business model of venture capital, and how it has increasingly taken on more of the characteristics of asset management. But the reality is that venture capital has ALWAYS had characteristics of asset management. When to raise money and how much is asset management. When to sell and how much is asset management.

These are critical and unavoidable parts of the job. But for a venture investor, the product you offer comes from Finding, Picking, Winning, and Supporting. Then, and only then, do you have the privilege of managing the assets around that engine you've built.

Thanks for reading! Subscribe here to receive Investing 101 in your inbox each week:

Love your very elegant explanation! Thank you!r

Such a great breakdown even if you're a founder. It's a great framework to evaluate VCs and where their strengths may be.