Capital Allocation Is Dead

The Analyst Is Dead. Long Live the Allocator.

This is a free weekly newsletter about the art and science of building and investing in tech companies. To receive Investing 101 in your inbox each week, subscribe here:

I’ve been investing for a little over a decade. In that time, I joke that I’ve had a Goldilocks experience of seeing a very different subset of investing across different firms. From regional seed investing as a scout at Kickstart to PE bargain hunting at TCV to big idea arbitrage at Coatue to venture classic at Index Ventures to, now, product-led venture at Contrary.

Over the course of that decade while I’ve seen a broad swath of investing, I had a buddy who started at a different firm around the same time. However, unlike me, he stayed at that firm for the full decade. So when he called me up recently, it was because he was finally picking his head up and considering a change. He figured I’d seen plenty of change while he’d seen none, so I would have some perspective.

What made the conversation so interesting, though, was that he didn’t just frame it as “I’m thinking about joining [other fund / this startup / starting this], what do you think?” Instead, he asked me where I thought the role of a capital allocator was going in a world turned upside down by AI?

Now, I’ve always been a proponent of a particular Flannery O’Connor-ism: “I write because I don’t know what I think until I read what I say.” But I’ve always found the same thing to be true of talking. Often, when given the opportunity to rant about something, I articulate a perspective that I’m not sure I realized I had. And that happened in this conversation when my first reaction was “capital allocation is dead.”

As I unpacked it, I took it from the more provocative version I started with and expounded on the idea to what I really meant. The programmatic, analysis-first way of allocating capital, the one a whole generation of investors were trained on, is over. It has been quietly dying for years, even though there’s still plenty of people who think it works. But, increasingly, not acknowledging how capital allocation has evolved is going to burn more and more investors.

Everyone’s An Allocator. The Analyst Is Dead.

The definition of investing I always come back to is “the art and science of allocating finite resources to create an optimal outcome.” Relatedly, I’ve written before about how everyone is an allocator of something; not just capital, but time, attention, love, energy. You allocate all day. So does your church, your city, your alma mater, your mom.

So the “allocator” part of capital allocation isn’t going anywhere. If anything, it’s the only part left. What’s really dying is the analysis-first approach.

There used to be a programmatic, analysis-first method of allocating capital, and by and large I don’t think it exists anymore. The style of investing that is, effectively extrapolation. You can take any business and you assume incremental growth, incremental margin improvement, incremental win-rate lift, incremental multiple compression as growth slows. You build a picture of what the business can be in ~5 years, why it can adhere to your return expectations, taper it responsibly, slap a multiple on the out-year, and back into a price. It was a beautiful machine. There were entire desks of very smart people at every firm who ran that playbook, and they were quite good at it. It was not a big-picture-first way of seeing the world. It was very much a sum-of-the-parts approach.

But I genuinely believe that the sum-of-the-parts machine no longer works, because capital allocation has become almost completely divorced from reality.

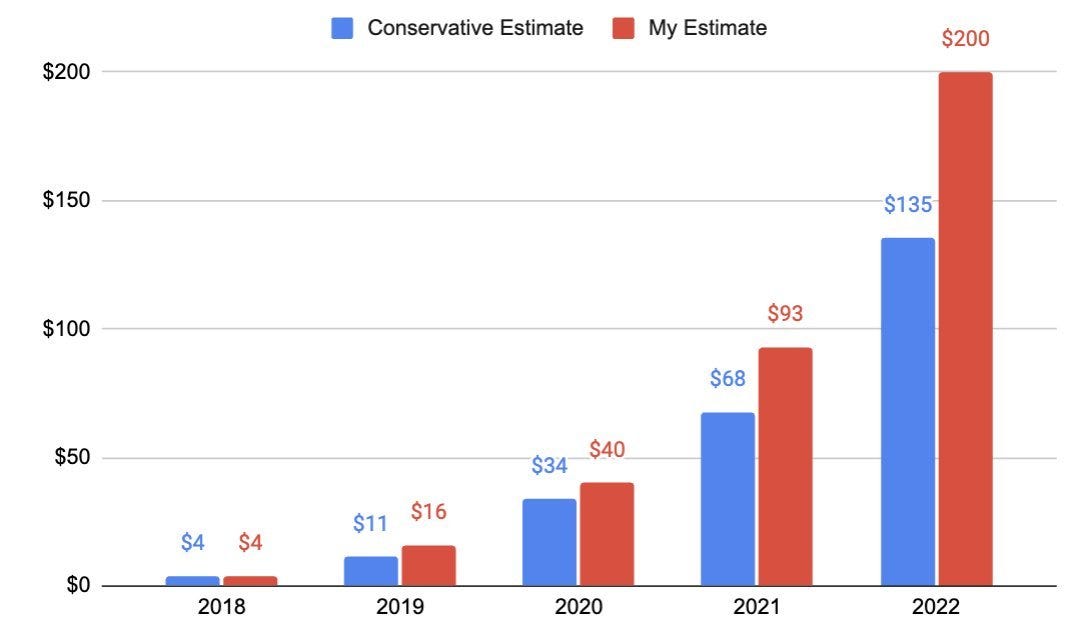

That sounds kind of doomery, but I’m not trying to just give up and declare investing as left for dead. There’s an element of that perspective that is just “markets are crazy.” But that’s not quite right. The better framing, I think, comes from a piece I wrote a few years ago called The Reality of Unrealistic Outliers. In it, I talked about a time when I had done a case study on Figma as part of a job interview in 2018. At the time, the company had $4M of ARR and Sequoia had just valued it at ~$400M. I had done a couple different exercises to think through how big Figma could get, and assumed that, by 2022, the company could hit $200M ARR.

My interview was with an analysis-first investor. He guffawed at my analysis, pointing to rules of thumb like “triple-triple-double-double-double.” By that logic, I had dramatically overshot what Figma was likely to do in growth.

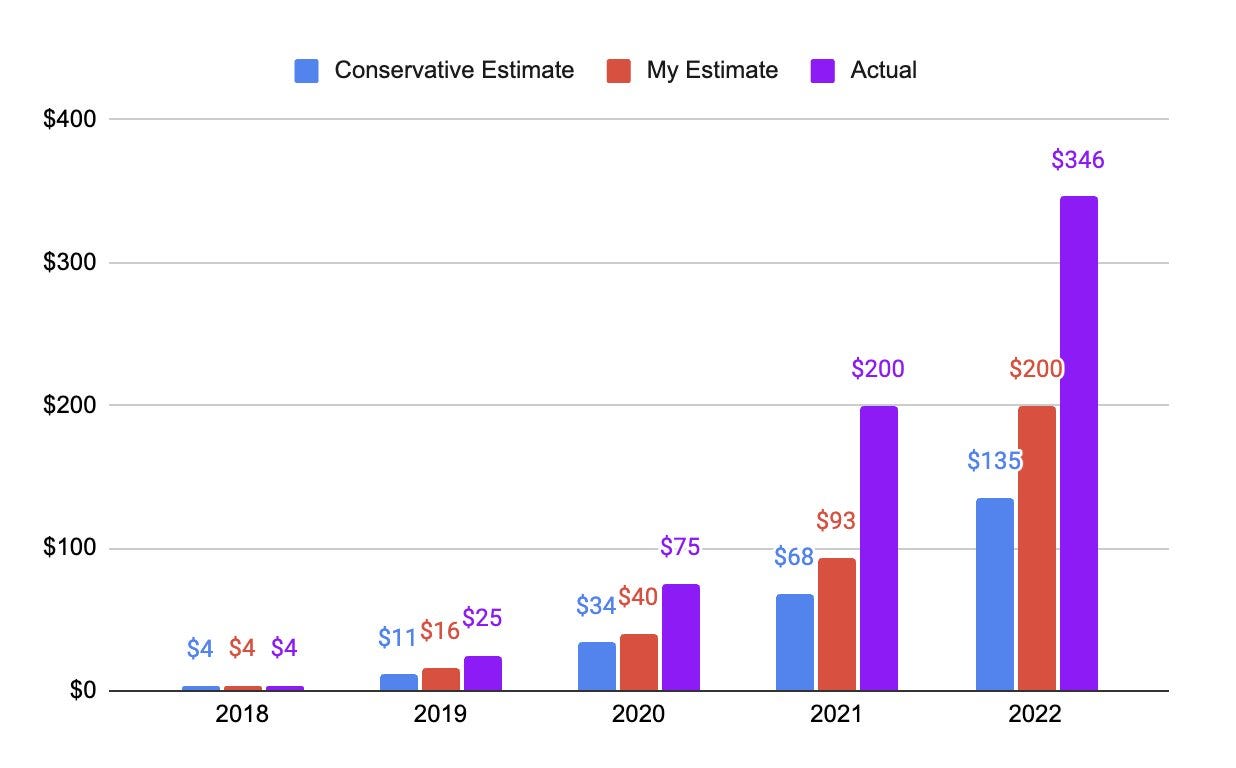

But, in reality, Figma dramatically overshot even my analysis, let alone the conservative “rule of thumb” this guy would have had me live by.

And that’s an example of a company that wasn’t just a hype narrative where the stock price was doing all the heavy lifting; it was a real company that was simply capable of executing well above expectations set by standard practice.

Thinking about those investing “rules of thumb” makes me think of a line in Walter Isaacson’s biography of Leonardo da Vinci about how he studied the rules of perspective so completely that “Once he knew the rules, he became a master at fudging and distorting them.” It’s a good example of how the “rules” aren’t necessarily wrong, but that its a mistake to believe the rules are reality.

The analyst’s whole religion is that the rules are the reality. That’s the religion that’s dead.

Four Ways To Aggregate

So if capital allocation isn’t being defined by analysis, then what is it? Here’s the reframe I gave my friend, and it’s the part I hadn’t said out loud before. What a capital allocator actually does now is aggregate assets around a particular strategy. And there are, as far as I came up with shooting from the hip in this 45-minute conversation, only four strategies really worth running. Four kinds of thing you can be good at aggregating. They are wildly different games, played by wildly different people, and very few people are even honest about which one they’re actually playing.

(1) You can aggregate quality. (2) You can aggregate narrative. (3) You can aggregate leverage. (4) You can aggregate time.

The Quality Game

The first bucket is the one everybody says they’re in. Quality Aggregators are trying to pull together the highest-quality assets in the world and let them compound: the best talent, the best compute, the best data, the best capital; the kind of capital with a high risk appetite that actually wants to be there.

This is the bucket I’m trying to build at Contrary. I want to be in the camp of finding the highest-quality people, the highest-quality ideas, the highest-quality operators, and bringing them together. Our particular flavor is born out of finding those highest-quality people just one notch before everyone else appreciates how special they are.

Here’s the thing people get wrong about this bucket right now, though. A lot of what looks like a 2021-style bubble is actually real in a way 2021 wasn’t. In 2021, a company would go from zero to $5M of ARR and get valued at a billion dollars. Generally, those were stupid investing decisions. Today you have companies going from nothing to a billion dollars of revenue in a year, and it’s not pretend, and (at least most of it? Some of it?) isn’t fraud. A good chunk of it is real. I fervently believe in the transformational power of AI, so much more than I ever bought into the cryptomania of 2021.

So much of AI skepticism rhymes with 2021 but that clearly misses the mark. The core crux of the debate shouldn’t be around whether its real, but about whether it has staying power. Passing judgement on venture hype is fine, and it can feel really good. Ask Ed Zitron; he’s clearly an AI-skepticism crackhead. But you’ll miss a LOT of real things if you default to that. Instead, the question you should be asking is all about defensibility. But defensibility is, typically, not something you can extrapolate from a comp set or determine from a margin profile.

If you want to play the Quality Aggregator game, then you have to have an incredibly high bar about aggregating the highest quality people who are chasing the highest quality ideas. From there, you can still expect 90% of them to fail (power law) but that 10% will build those “Unrealistic Outliers” that seem to defy the laws of gravity when it comes to building exceptional businesses.

The Narrative Game

The second bucket is the made-up one, and I mean that as a compliment. Narrative Aggregators aggregate story. Hype. The right heat around the right thing at the right moment. A lot of it is very pretend and feels very 2021. But some of it is the single most valuable asset in the world right now, and pretending otherwise is how analysts go broke.

I’ve written over and over about storytelling, because for a long time I believed reality was more important than narrative, and I’ve slowly become convinced that narrative controls reality. Ask a hedge fund analyst what a company’s valuation is based on and he’ll say the future cash flows. Ask a VC and the answer is different: “The narrative.” I’ve said before that hype is a physical force that deserves a place on the periodic table, that its social and economic impacts are as powerful as oxygen or hydrogen. I meant it literally.

Take SpaceX. If you unpacked the enterprise value, maybe 10% of it is high-quality assets you could touch, and 90% of it is narrative. That doesn’t make it fake. Plenty of narrative assets eventually materialize into quality assets. It just means the story is doing most of the lifting, and the story is the actual asset. There is no world where SpaceX, as a rocket launch company, is worth two trillion dollars on the numbers. It’s worth two trillion dollars because of the hype, and the hype is a real force.

And Elon has crafted the perfect narrative for this moment in time. The SpaceX + xAI (e.g. Colossus) + Cursor is an exceptional AI behemoth narrative to weave. Side note: I can’t even fathom the capital destruction event that would happen if Elon Musk died from a heart attack tomorrow. Talk about key man risk! But while he’s at the helm, the narrative shines through!

This is why the people who short Tesla get destroyed. On the numbers, they’re right. Tesla does not bear the weight of its valuation, and they can prove it to you line by line. But they don’t understand hype as a physical force of nature, so they get rocked. Being right on the analysis and wrong on the narrative would only work if you got participation points, but in markets it’s just a full loss.

Now, I’ve always struggled with Narrative Aggregation as a strategy. The way I’ve said it before is “you can’t eat narrative.” A story with nothing underneath it is just the institutionalized belief in a greater fool; the assumption that some bag-holder down the line will believe what you can’t quite bring yourself to buy into. The Narrative Game has plenty of hucksters and jabronis; it’s where they thrive! But the high-brow Narrative Game isn’t “believe anything.” It’s knowing “which stories will actually materialize, and that the story itself is a real, ownable, price-moving asset in the meantime.” Those are two different skills, and you need both.

The Leverage Game

The third bucket is my favorite to think about, even though it isn’t the one I’m running. Leverage Aggregators don’t chase the highest-quality assets or the hottest narratives. They find high-leverage assets: distribution, vertical-ownership, stickiness, the boring things that quietly moves the needle. The whole game is buy good assets, leverage the synergies inside the network of assets, and profit.

I know the quintessential version of this person. A guy I worked with in a prior life left our old firm and started a HoldCo; real balance-sheet capital, not a fund. The whole thesis is that niche verticals are under appreciated, and I’ve become more and more convinced he’s right. The internet has supercharged niches. There’s a woman on TikTok with a million and a half followers who clears half a million dollars a year, and all she does is mushroom foraging! Riches in niches turned out to be real.

His first acquisition was equestrian software. A tool for horse trainers. The company was a nice little business, quite profitable, though not growing super fast. They went in, professionalized the sales team, went upmarket into the enterprise horse-training operations, and it’s now dramatically larger and still exceptionally profitable. And they own 100% of it. The next one was funeral-home software. Three sleepy players, none of them hungry, so he bought all three, put them together, and now you have pricing power none of them had alone. This is the same engine that runs Constellation Software.

Deal junkies are the hucksters of this particular game, and that’s what separates the good version from the garbage version.

The garbage version is the Jack Welch playbook: big money moving big money around, stapling two logos together, calling it synergy. Most of those deals suck. They just look good. Welch’s own investor-relations team, in David Gelles’ telling, wasn’t selling products, they were “selling a narrative.” Sometimes Leverage Aggregators work for Narrative Aggregators (e.g. the deal guys that helped Elon buy Cursor were those two playbooks working off each other). The difference between Jack Welch and Elon Musk is that Welch’s GE never actually delivered anything; all sizzle, no steak. Elon’s businesses, while having narrative eon’s ahead of their visible reality, does actually deliver earth-shattering outcomes every now and then. Welch was narrative pretending to be leverage. Elon is leverage wrapped in narrative. One is hollow, while the other is just expensive.

But the purest version of Leverage Aggregators doesn’t need a story at all. Think about Bending Spoons. They buy mature, unloved software: Evernote, WeTransfer, Meetup; apps that had drifted, and they run them with a discipline the last owner never brought. Nobody is pitching you a trillion-dollar future. There’s no narrative to buy. The entire edge is that they know what good bones look like, they buy them cheaply, and they have a repeatable machine for getting more out of the same asset than anyone else can. Those acquisitions don’t have to be heroic or Herculean, its just a repeatable leverage play that you can run again, and again, and again on the next boring, unloved thing.

In fact, the very best Leverage Aggregators start from a worldview, not a spreadsheet. There’s a PE shop that spent 25 years quietly buying up the best operators in nuclear servicing: waste handling, transportation, asset maintenance. A whole category everyone else had written off as toxic and shrinking. On the numbers, every one of those businesses is high-risk, highly-regulated, going-nowhere revenue. The analysis-first allocator would pass. Or maybe buy one and harvest the margins. The only way you patiently assemble the entire set over two decades is if you believe, ahead of the math, that nuclear comes back and that owning the whole ecosystem is worth more than owning any single piece of it. They were right. It’s now a multi-billion-dollar business they own outright. The leverage was never in the assets. It was in the thesis that let them see the assets differently than everyone else did.

And notice: you cannot analyze your way into any of these. On the numbers, the equestrian software company is a “harvest it and move on” at best, and a “pass” at worst. The only way you do that deal is if you already believe, before the model, that verticals are under appreciated. The worldview comes first. The math is downstream.

The Patience Game

The fourth bucket is the one I respect the most and am the least good at. Patient Allocators aggregate time. They find a good-shaped asset, park capital in it, and then do the hardest thing in the business, which is nothing.

The best of them are honest about what they are. They’re not the founder, not the deal sniper, not the genius operator. They’re the parker. One of my own LPs runs a multi-billion-dollar industrial holding company, and the guy who does their allocation is just very focused on seeing a good-shaped asset and putting money there and waiting. The Larry H. Miller family sold their dealerships and sat on something like $9B in cash, and their CIO has quietly done beautiful things with it. Sequoia Heritage built a veterinary-clinic chain from scratch nine years ago that now does about a billion in revenue.

Sequoia Heritage, in particular, is a great example of strategies that can find the same outcomes through different ways. Their vet-clinic chain is sitting right next to their SpaceX and ByteDance positions, but the point is that they entered SpaceX at something like a $15-20B mark. Rather than them being in the game of aggregating the high-quality assets that birthed the thing, they’re saying “this is an asset that ought to be owned, and I have a seat that lets me own it semi-permanently.”

The Church of Jesus Christ of Latter-Day Saints has built a $200B+ empire playing the long-game. They saw humanitarian needs post-WWII and realized how valuable it is to actually be the owner of the underlying asset, so they bought cattle, citrus land, etc. “We are constantly at the mercy of the landowner, so we ought to just be the biggest landowner of the thing we need most.” But, beyond that, they also looked for other positions to park capital in, like Nvidia and Google in 2019.

This is the Buffett game. And, for the passive observer, its important to note that Buffett isn’t actually a value investor, regardless of the cigar-butt mythology lore. He said himself that puffing on a cigar butt and tossing it out was “a rat race” and “unsatisfying.” One of his critics once summed up his career as three careers: “In the old days, he was a scavenger. He looked for value. Then it got hard to find stuff and he became a franchise investor; he bought great businesses at reasonable prices. And then he said, ‘I can no longer find good businesses at even acceptable prices, and I will take advantage of my size and teach the world a lesson about long-term investing.’” His money didn’t come from Ben Graham. It came from Apple and Coca-Cola, from identifying companies with a special something and being willing to wait decades. As Munger liked to quote Livermore, “the big money is not in the buying and selling, but in the waiting.”

Which brings me to the cardinal sin of this bucket, and the cleanest proof that the analyst is dead even here. Mohnish Pabrai is about as pure a Buffett-and-Munger disciple as exists. He paid six figures for a charity lunch with Buffett, wrote the book on concentrated value investing, and at one point had something like 77% of his entire fund sitting in a single stock: Micron. He’d held it since 2017. But then, in 2023, right before the AI-memory boom, he sold the whole thing. Over the next two years Micron ran more than 15x, and the exit is estimated to have cost him around $2B in gains. He got wrecked. And not because he missed the semis narrative, it was clearly a bottleneck. Not because he misjudged Micron as some tier-one asset, cause it really wasn’t one. He got wrecked because, in the end, he played the Patience Game like an analyst. He talked himself out of a position that only needed him to sit still. The whole job was to do nothing, and the analyst brain really struggles to do nothing. The analyst is prone to over-analyze.

The Analyst Gets Demolished

So here’s the whole thesis in one picture. Take that same analyst, the one running the beautiful sum-of-the-parts machine, and drop him into each of the four buckets. Watch what happens.

In the Patience Game, he baselines. He does roughly fine, because the game is forgiving and mostly just requires sitting still, which he’ll ruin sometimes but not always. In the Leverage Game, he underperforms, because he passes on the equestrian software or buys it and harvests it, never seeing the vertical expansion opportunity. In the Quality Game, he loses, because he keeps underwriting the best assets to a responsible-looking out-year and the best assets don’t do responsible things. And in the Narrative Game, he gets demolished, because he shorts the Teslas and SpaceXs of that world, and never understands he was standing in front of a physical force, wholly illogical.

It’s a sliding scale. The further up the curve you go, from quiet quality to pure narrative, the worse the pure analyst does, from mild underperformance to total annihilation. And the reason is the same in every bucket. Analysis, at its core, is extrapolation. And with the best things, extrapolation is always wrong, and always wrong on the low side.

There’s an exceptional excerpt from Sebastian Mallaby’s book, Power Law where he explains the exact weakness of extrapolation:

“A huge amount of energy in government, financial houses, and corporations is spent on forecasting the future, mostly by running statistical analyses on patterns from the past; without a clear forecast, committing resources would seem irresponsible. But the way venture capitalists see things, the disciplined calibrations of conventional social scientists can be a blindfold, not a telescope. Extrapolations from past data anticipate the future only when there is not much to anticipate; if tomorrow will be a mere extension of today, why bother with forecasting? The revolutions that will matter—the big disruptions that create wealth for inventors and anxiety for workers, or that scramble the geopolitical balance and alter human relations—cannot be predicted based on extrapolations of past data, precisely because such revolutions are so thoroughly disruptive. Rather, they will emerge as a result of forces that are too complex to forecast—from the primordial soup of tinkerers and hackers and hubristic dreamers—and all you can know is that the world in ten years will be excitingly different. Mature, comfortable societies, dominated by people who analyze every probability and manage every risk, should come to terms with a tomorrow that cannot be foreseen. The future can be discovered by means of iterative, venture-backed experiments. It cannot be predicted.”

Or, as Buffett put it more bluntly, “the forecasts may tell you a great deal about the forecaster; they tell you nothing about the future.”

So if analysis is dead, what replaces it? I did a podcast recording a couple days ago where the final question was “what advice would you give to people who want to be pioneers on new frontiers?” My answer to that question is the same as what replaces analysis. A worldview.

The Quality Aggregator believes the best assets break the “rules of thumb.”

The Narrative Aggregator believes the story is the asset that controls reality.

The Leverage Aggregator believes the world is made up of under appreciated assets.

The Patient Allocator believes the big money is in the waiting.

The best investors ask “what do you have to believe,” and then answer it with specificity, because believing, actually believing, is being able to articulate what you have to believe and why.

Therefore, What?

I told my friend all of this, and then he asked the fair question. So what does that mean for me? For the shops I’m interviewing at, the big platforms that have become aggregators of strategies and asset classes, all of them still fundamentally analysis-first about software?

Here’s what I actually believe. Firms will change faster than even they expect, and being analysis-first isn’t a home you can keep. The good analysts have two honest exits, outside of the slow spiral into irrelevance.

They can stay analysts and become downstream capital, the very good people you want dotting the i’s and crossing the t’s on a $70B take-private, like Stripe working with Advent to buy PayPal. Those deals require real work done by real skill. But they’re a services business, not an edge. The real Leverage Aggregator is the deal guy INSIDE Stripe pushing to buy PayPal.

Otherwise, analysts will have to find a worldview: roll up a vertical, back a thesis nobody believes yet, become a Leverage Aggregator or a Patient Allocator or one of the emerging Quality Aggregators. Any of the four can be a great life. What’s not a great life is running the sum-of-the-parts machine and calling it investing while the ground moves out from under you.

And the one thing I’d guard against, for him and for me and for you, is getting hype-sniped. I had a friend once who read Poor Charlie’s Almanack right alongside me for years, but then went all-in on NFTs as the future in 2021. I mostly stopped talking to him. Granted, AI is not that. AI is far more real than crypto ever was. But precisely because so much of it is real, the hype is more dangerous, not less, because it’s harder to see the edge where opportunity falls off into pure hype. Two things are certain at once, and both can be true: some of these companies will be the most powerful value-creators of our lifetime, and a very large percentage of them will turn into carnage. The whole task is telling those apart, and you will not do it with a model.

So pick your bucket. Quality, narrative, leverage, or time. Then go get a worldview worth having, because the numbers can no longer have one for you.

The analyst is dead. Long live the allocator.

Thanks for reading! To receive Networked Conviction: My Investing Journal, a collection of portfolio updates, Requests for Startups, and investing ideas for paid subscribers, you can sign up below: